Since 2000, by all metrics, greenhouse gas (GHG) emissions due to industry have risen more quickly than from any other sector, accounting for 14.1 GtCO2eq (gigatons of CO2 equivalent) in 2019, 24% of the world total, second behind the energy sector (20 GtCO2eq/34%). Achieving net-zero emissions from industrial sources is a huge but not impossible challenge. The main avenues for this are electrifying processes and switching to low- or zero-carbon energy sources, and finding low-carbon feedstocks.

All illustrations from the IPCC 6th Assessment Report, Vol. 3, Chap. 11. Aspects of decarbonizing industry.

Industrial greenhouse gas (GHG) emissions, 1900-2019.

Among all types of physical stock bought and sold for industrial purposes, plastics have grown in use the most quickly since 1970. We depend on petroleum for more than 99% of feedstocks for plastic. Meanwhile we don’t recycle much and industrial processes emit large amounts of GHGs. This is one of the most difficult and essential areas for improvement in the entire range of mitigation scenarios.

Industrial feedstock demand, 1970-2019.

Industrial GHG emissions, 1970-2019, by world region.

It requires changing the frame of reference from small, incremental increases in efficiency, to a complete reimagining of some aspects of manufacturing (not unlike in the building sector, switching from efficiency to sufficiency). Scaling up newer, less GHG emissions-intensive manufacturing processes, and broadening the use of electricity (as we decarbonize the electricity sector) are within our capabilities now. Estimating the cost is difficult, however, because many aspects of pricing interact in, to use a mathematical term, nonlinear ways, where a single price adjustment will have several cascading effects, including on itself. While it’s easy to see the hesitancy of industrialists to retool, given this uncertainty, the growing certainty of climate-related disaster is changing the equation (to keep things math-y).

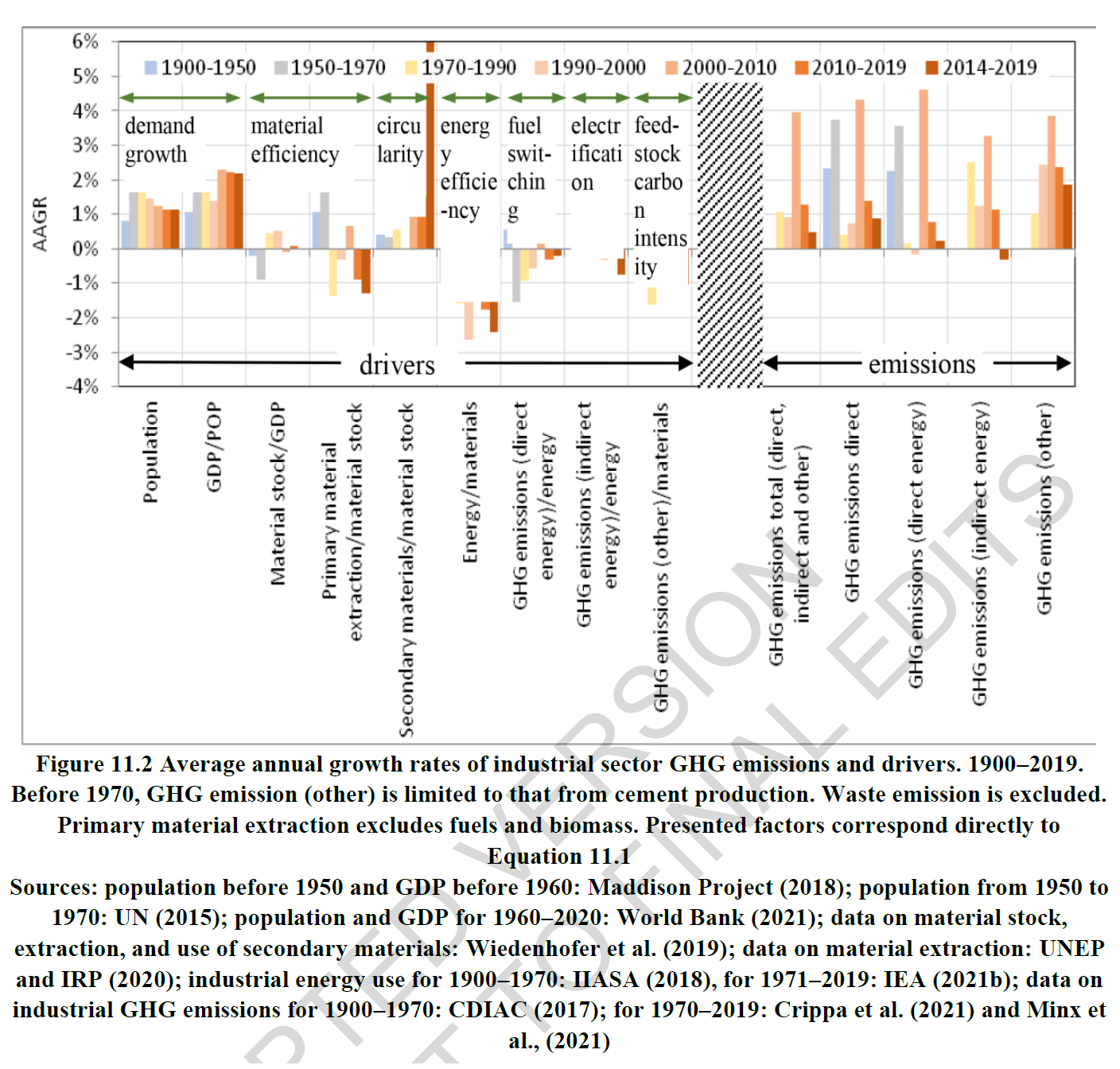

Industrial GHG emissions, 1970-2019.

The feedstock reliance on petroleum can be largely mitigated through use of biomass carbon (such as biomethane and methanol) and recycled materials. The question of who bears the costs for less emissions-intensive carbon sources is thornier. With sufficient innovation and scaling, costs for these alternate sources could be lowered from their currently high price.

Industrial GHG emissions, 1970-2019, by world region.

World demand growth for various materials, 1990-2019.

However, the experience of the post-COVID environment has shown the world that large companies are all too willing to price goods oppressively. As with the difficulty of inducing behavioral change in people to consume and travel less, damping the profit motive in for-profit corporations is a bigger challenge than any technical issue. Bringing such a revolution about in industrial processes and pricing will require social and governmental action.

Material efficiency strategies.

Strategies for decarbonizing industry.

The use of concrete is frequently ignored in carbon budgets,

because the materials for making it are cheap and easy to find. Concrete is

overused because it is inexpensive and durable. Improved fabrication methods

and more sparing use—only where concrete’s mechanical properties are needed—could

reduce CO2 emissions from this sector of industry 25-50% by 2050.

But again, as in the case of alternate, more expensive feedstocks, the hurdle

is asking developers to use more expensive, mechanically weaker alternatives

where concrete is not necessary.

Toward low-carbon plastics.

GHG emissions for various scenarios and aspects of industry to 2100.

A fair amount has been written on the geopolitical implications of renewable energy, with renewables-rich countries potentially becoming energy exporters (meanwhile, a prominent oil exporter like Saudi Arabia will remain important because inexpensive oil will remain economically necessary for several decades. But renewables have geo-economic impacts too, in terms of availability of renewable energy for industrial operations around the world. Developing countries, which can now simply import coke, coal or oil to fuel their growing manufacturing bases, would face a far more difficult tasks in building a parallel renewable energy industry alongside the manufacturing. Regional availability of low-carbon electricity is another huge challenge in decarbonizing industry.

Materials life cycles, mitigation and policies.

Tomorrow: national and sub-national policies and institutions.

Be brave, be steadfast, and be well.

No comments:

Post a Comment